Answers for Long-Term Challenges

Feb 20, 2025

The Seattle Times reported recently on challenges facing Washington state’s long-term care program, Washington Cares.

It is no surprise. Government has been unsuccessful in running long-term care insurance programs including the Medicare Catastrophic Coverage Act of 1988, part of President Clinton’s health reform in the 1990s, and the Community Living and Assistance Services and Support Act, part of the Obama administration’s Affordable Care Act.

As states consider implementing public plans like Washington Cares, which funds only a small portion of an individual’s potential long-term care needs leaving significant gaps in coverage, success would be more likely if such programs are integrated with private long-term care insurance options. This helps ensure people can access coverage when they need it.

In the private market, long-term care insurance remains in effect regardless of one’s state of residence. But a Washingtonian who relocates out-of-state loses access to the coverage offered in the current Washington plan.

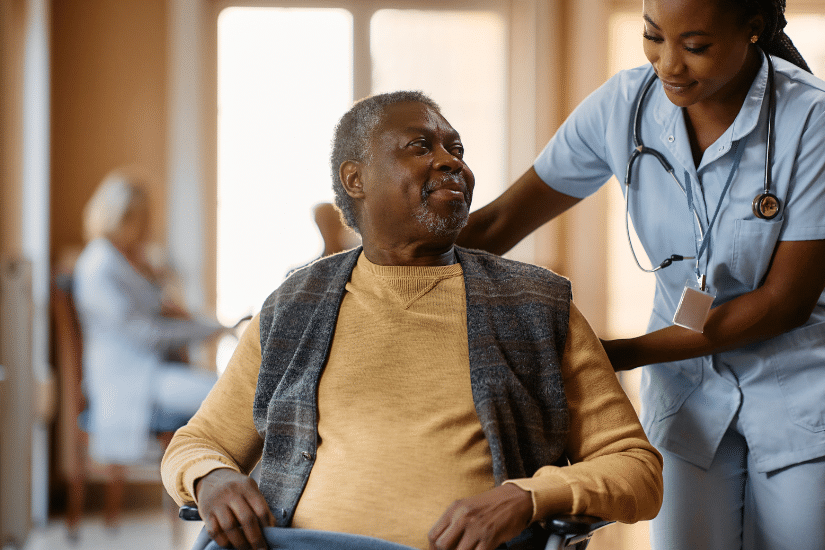

Nearly 70 percent of 65-year-olds will face the need for financial protection against the high cost of long-term care. Fortunately, long-term care insurance is widely available in a range of prices and benefits, with the greatest growth – about six times — over the past 10 years in combination products. These combine life insurance or annuity products with a long-term care option.

All policies – whether combination products or traditional “standalone” long-term care insurance, typically cover care in nursing homes, community and assisted-living facilities, and at-home services. COVID-19 has highlighted the importance and popularity of at-home care, though it can be expensive at approximately $4,500 monthly. Long-term care insurance can defray all or part of the cost of needed long-term care services.

November is National Long-Term Care Awareness Month.

It’s important to know that an individual who obtains coverage will always have it as long as premiums are paid. A policyholder never has to worry that declining health will lead to policy cancellation, or an increase in premiums.

Low-income Americans needing long-term care generally can access help through Medicaid. But for other Americans unable to self-fund long-term care costs, private insurance represents the best route to long-term care financial protection.

Jan Graeber is Senior Actuary at the American Council of Life Insurers (ACLI). She is responsible for industry advocacy on long-term care, risk classification, and supplemental benefits before federal and state policymakers, the National Association of Insurance Commissioners, and other groups that influence insurance policy, laws and regulations.