Retirement Readiness Tops Middle-Class Americans’ Financial Goals

Jun 10, 2026

As previously discussed, the United States is in a low interest rate environment. Low interest rates negatively impact people saving for retirement, including those who invest in fixed-return assets (assets that pay people a set interest rate). They can have a particularly severe impact on retirees and those nearing retirement.

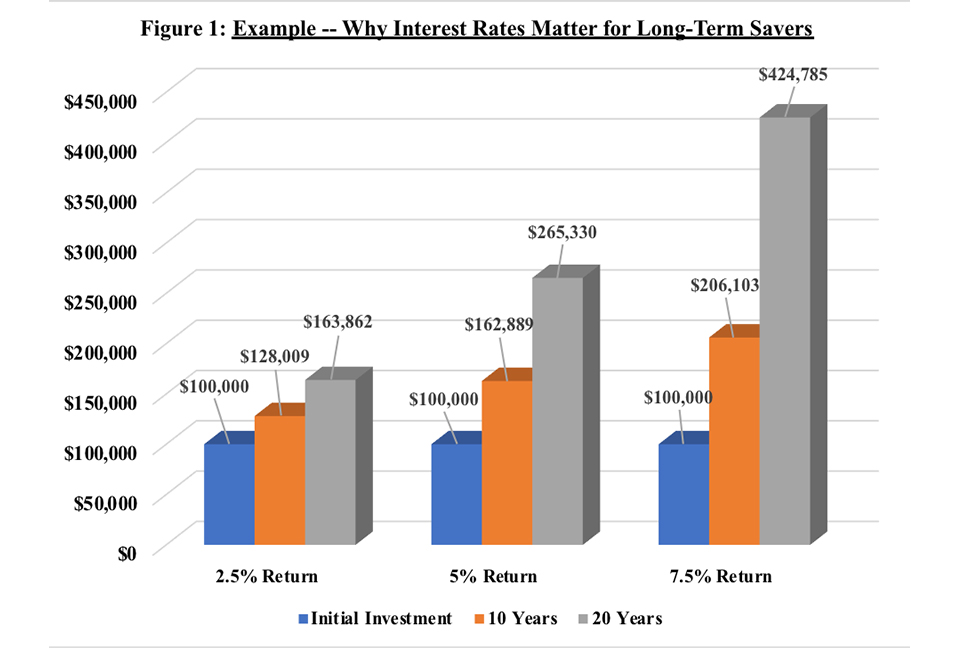

But how much do a few percentage points really matter? Consider two simple examples:

1) A 50-year-old invests $100,000 in a fixed-return asset that pays 2.5%, compounded annually.

If she holds the investment for an additional 10 years, the difference is even more stark.

2) A newly retired 65-year-old saved $500,000 with which he intends to fund his retirement. He plans on withdrawing $50,000 annually to supplement his Social Security income and a lifetime annuity that he owns.

In this example, a five-percentage point difference means more than five additional years of retirement income. Given that the typical 65-year-old can expect to live to age 85 (half will live longer), five years represents one-quarter of his hopeful retirement.

The real world is more complicated than these simple examples. For the sake of brevity, we assumed away several important things. And there are key products like annuities that can ensure a steady income throughout retirement. But the main point is clear – interest rates matter for retirement savers and retirees!

Andrew Melnyk is Vice President, Research and Chief Economist at the American Council of Life Insurers (ACLI). He holds a doctorate in economics and is a Certified Business Economist. His functions at ACLI include authoring white papers; managing the production of statistical publications; and managing ACLI’s Research Department. Prior to joining ACLI in 2005, he held positions in academia, government, and the private sector, both in the U.S. and abroad.